Do you know how the government calculates its Deficit?

The overall fiscal position of the Government can either represent a surplus or a deficit. A surplus occurs when the Government collects more revenue than it spends and a deficit occurs when spending exceeds revenue. In the Supplementary Budget, the FY2021/22 deficit is estimated at $858.6 million, down from the earlier estimate of $951.8 million and lower still from the FY2020/21 deficit of $1,348.1 million during the worst of the COVID-19 pandemic.

How does the Government calculate the deficit?

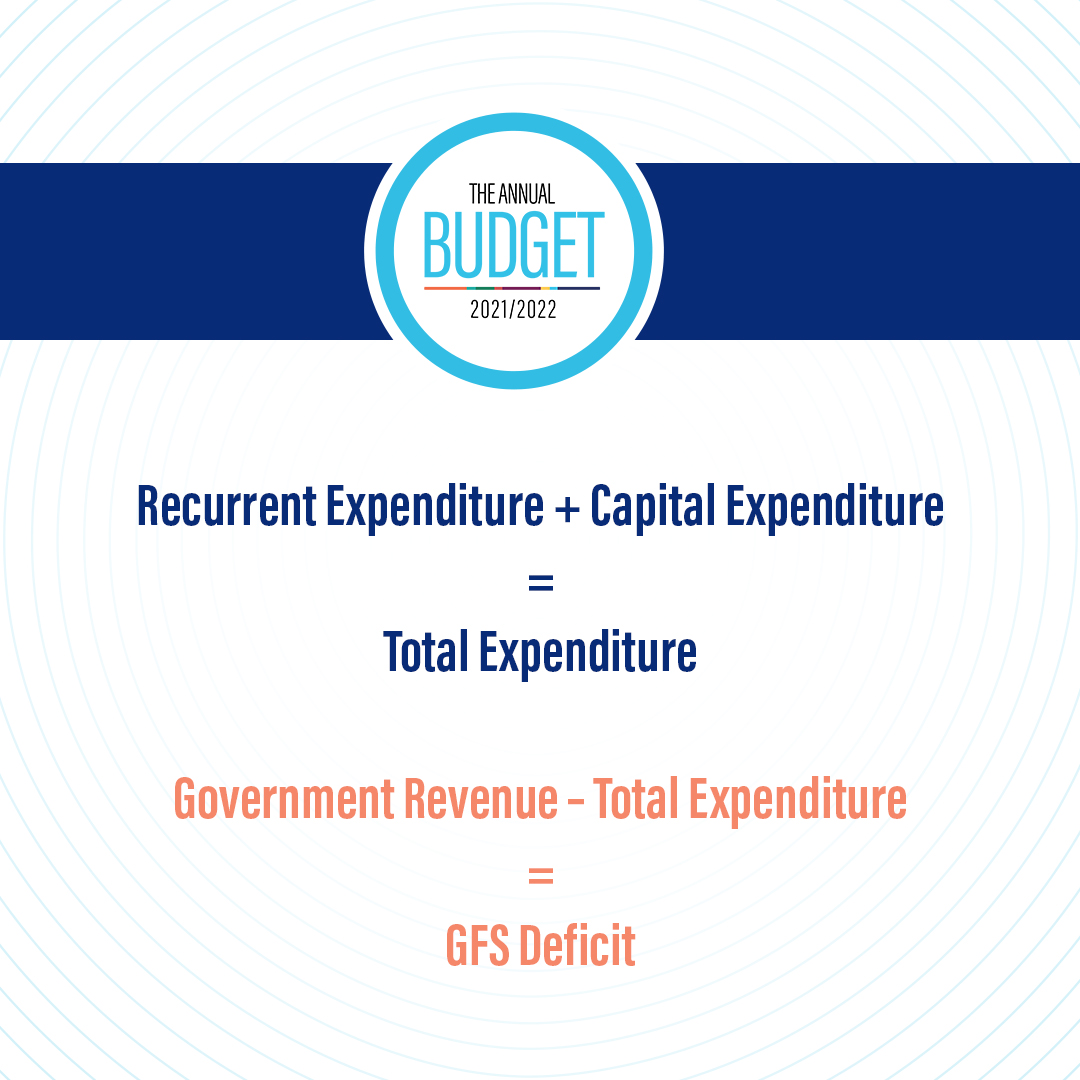

The Government Finance Statistic (GFS) deficit is calculated by adding recurrent expenditure to capital expenditure. The total of recurrent and capital expenditure is subtracted from Government revenue. This calculation is in keeping with the IMF’s Government Finance Statistic methodology. Using this method, while interest payments are included as an expenditure by the Government, borrowings and repayment of debt are accounted for during the fiscal period in which they were recorded as financing activities and hence are not included as expenditure items.

Original Calculation

Before FY2018/ 2019, recurrent expenditure included the cost of debt repayment. To calculate the recurrent deficit, recurrent expenditure was deducted from government revenue. Capital expenditure was then subtracted from the recurrent deficit to amount for the total deficit amount. However, prior to FY2018/2019, the cost of debt repayment was included in recurrent expenditure, so this amount was added to the total deficit to arrive at the correct Government Finance Statistic (GFS) deficit.

New Calculation

Using the presentation adopted since FY2018/2019, the cost of debt repayment has been excluded from recurrent expenditure, simplifying the calculation. The GFS deficit is now calculated by adding recurrent expenditure to capital expenditure. The total of recurrent and capital expenditure is subtracted from government revenue, resulting in the same GFS deficit amount as before.

This change in presentation is in keeping with the IMF’s Government Finance Statistic methodology. In this method, while interest payments are included as an expenditure by government, borrowings and repayment of debt are accounted for during the fiscal period in which it was obtained as financing activities and hence are not included as an expenditure item.

See this example from FY2016/2017

|

Fiscal Summary 2016/17 |

||

|

|

Original presentation |

New presentation |

| Recurrent Expenditure | 2,320 | 2,033 |

| Recurrent Revenue | 2,175 | 2,175 |

| Recurrent Balance | -145 | 142 |

| Capital Expenditure | 242 | 242 |

| Capital Revenue | 0 | 0 |

| Capital Balance | -242 | -242 |

| Total Deficit | -387 | -100 |

| Debt Redemption | 287 | 0 |

| GFS Deficit | -100 | -100 |

Source: Draft Estimates of Revenue and Expenditure 2016/17